Playing To Win

Dangerous Cost Reduction Projects

Dis-Integrating Strategy is Always a Bad Idea

Recently, a client asked for advice on which of three consultant proposals to accept for a large corporate-wide cost reduction project. My advice was “d) none of the above” — unless the consulting firms made one specific modification. Since this kind of work has become a huge line of business for the consulting giants, I thought it would be useful to tackle the subject in my 41st Year III Playing to Win/Practitioner Insights piece Dangerous Cost Reduction Studies: Dis-Integrating Strategy is Always a Bad Idea. You can find the previous 151 PTW/PI here.

The Background

In the past decade, one kind of study has become a huge and highly attractive line of business for the so-called ‘strategy consulting’ giants, including but not limited to McKinsey, BCG, and Bain. These are cost reduction projects in which a major portion of consultant compensation is in the form of ‘gainsharing’ of the cost reductions identified — typically between $1 in fees for every $5-$7 ‘saved.’ This is an awesome form of compensation for consultants, who are used to billing based on time spent. It is largely uncapped and free from justification based on number of person-months of work performed.

These consultants have borrowed the specific compensation structure from ones use to the provider’s benefit across the professional services domain. The winning model is to contract for a share of a large pile of cash that the client currently doesn’t have but you will help it get.

Capital underwriting is a perfect example. The investment bank says to the client: “Wouldn’t it be nice to have a big pile of new equity — say, $950 million of it.” Client: “Why not a round number?” Investment bank: “Oh, it is because we are going to sell $1 billion of shares to investors and keep $50 million as our fee.” The client thinks: “Fine. Even though there is absolutely no justification for a fee of that magnitude, we are paying it out of money that we don’t currently have, and we won’t get the $950 million if we don’t pay the $50 million. Happily, the $50 million doesn’t need to come out of any existing budget.”

Trial lawyers who charge contingency fees — i.e., a percentage of the award/settlement but only if successful — are the same. The client pays a ridiculously huge percentage of the award or settlement, and the trial lawyers get so rich that their industry is the biggest lobbyist in Washington because it is critical for the trial lawyers to keep the contingency fee structure in place.

Why it is Dangerous?

The fundamental flaw in these cost reduction projects is that while revenues and costs are an integrated whole, these projects implicitly assume that costs can be reduced with no meaningful negative impact on revenues — and these gainsharing agreements absolve the consultant of any responsibility whatsoever to pay attention to revenues. They get paid for cost reduction regardless of its collateral impact on revenue reduction. There could be two dollars of revenue reduction for every dollar of cost reduction, and the consultants would still get paid — and handsomely.

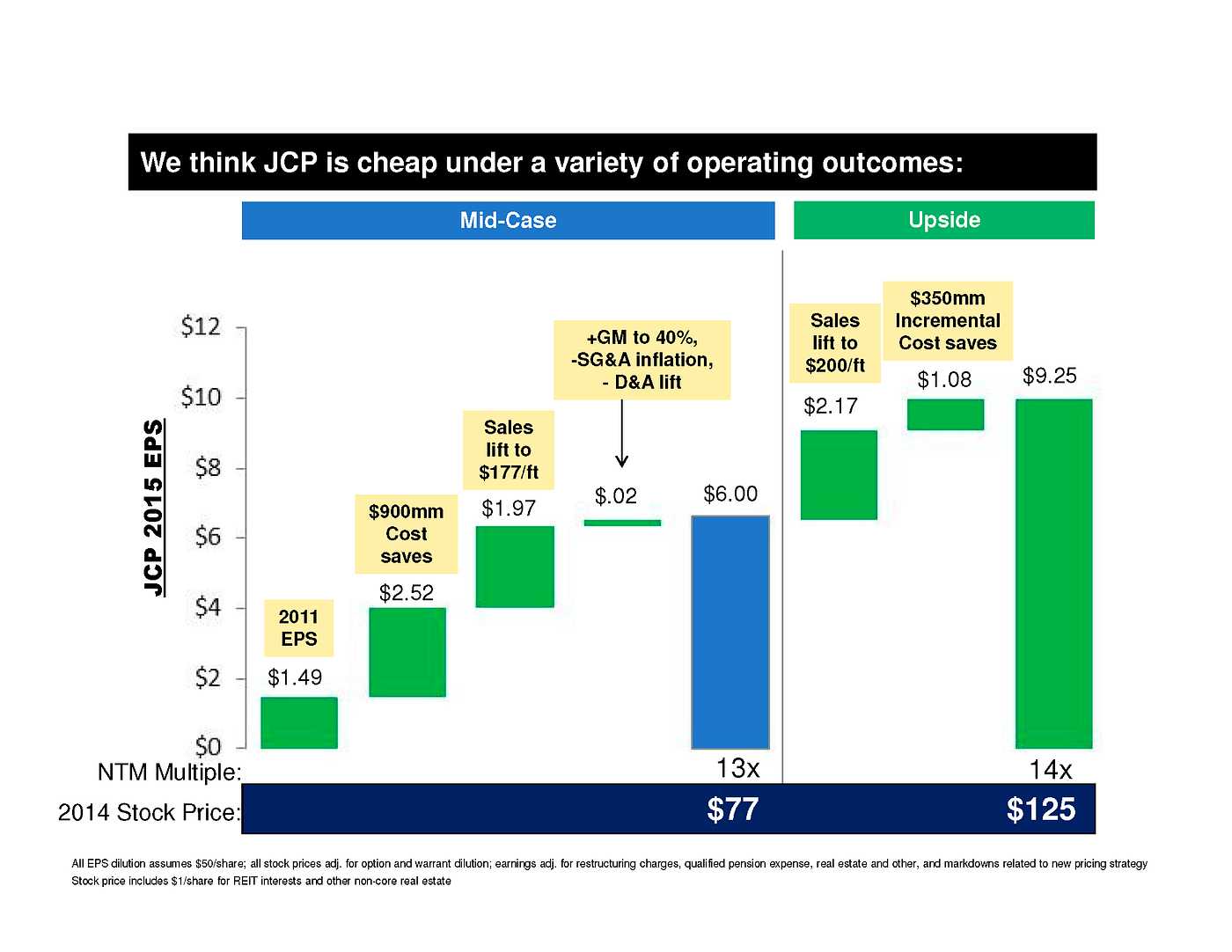

The chart above illustrates the dis-integrated mindset. It is from a Pershing Square presentation on May 16, 2012, called ‘Think Big.’ Bill Ackman is (in)famous for his PowerPoint decks extolling the virtues of his hedge fund’s insights on how to dramatically increase the profitability of his hapless target — in this case JC Penney — over what its obviously pathetic management is currently doing. Clearly, management is thinking small, not big, like Ackman!

The decks always contain the above sort of chart that builds up from the current profitability (here expressed in EPS) to a wonderful new profitability based on Pershing Square brilliance. In this case, it includes $3.60/share in cost reductions on an initial base of $1.49 — meaning a resultant EPS of $5.09 (over triple the base, plus a bunch of other fantasies to achieve $9.25/share).

The implicit assumption behind the chart is that the $1.49/share base is completely solid such that every dollar of cost savings adds a dollar to earnings. Unfortunately for Pershing Square, after four years of its brilliant ‘Think Big’ management, EPS wasn’t $9.25 or $5.06 or even $1.49. It was a big negative. And the stock wasn’t at $125/share or even $77/share or even the $25/share at which Pershing Square bought in. Instead, it had to unload its stock at about $12/share and absorb a loss of $470 million. The base wasn’t solid. Through all Pershing Square’s supposedly brilliant moves, sales/square foot plummeted. You can take out all the costs you want but if you aren’t paying attention to the impact on revenues, you are attempting to catch a falling knife — and Pershing Square experienced just how bloody that can be.

The same happened to Brazilian private-equity firm 3G Capital when it took control of Heinz then Kraft and engineered a merger of the two food companies (as I discuss in my book When More is Not Better). 3G immediately went about hacking at what it saw as a bloated cost structure, cutting SG&A costs from 10% of sales to 8% of sales between 2015 and 2018 — an impressive 20% improvement in overhead-cost efficiency. However, over the exact same period, gross margin fell by 3.5 percentage points, from 39.5% of sales to 36% of sales.

The base was anything but solid. Yes, SG&A fell by 2 percentage points, but that helped to drive a reduction of margin by 3.5 percentage points, a net negative of 1.5 percentage points, which forced Kraft Heinz to announce a $15.4 billion write-down in its assets in 2019, one of the ten largest corporate write-downs in the decade.

I have watched fallout like this too many times. Not too long ago, a CEO client of mine left his company to become the CEO of another large public company. He arrived to find that previous management had contracted with one of the prominent ‘strategy consulting’ firms for a gainsharing cost reduction program that had cost it over $200 million over the prior 24 months. Had it resulted in performance improvement? Sorry: not at all! That is why the board fired the CEO and hired my client, whose observation was that his company was in strategic shambles and had to start from scratch to repair the damage done. One of his first tasks as CEO was (with the help of his CFO) to meet with the Managing Partner of the consulting firm and negotiate a settlement to get out of the disastrous gainsharing deal. That is but one of many such deals that I have watched hobble companies.

The Unlearned Lesson

The lesson from these and innumerable other cases ought to be that a company should never give anyone, let alone a craven third-party, a naked, unidimensional incentive to cut costs. Anybody of even modest talent can cut costs if they don’t have any responsibility for revenues. At a payoff of $1 per $7 saved, I could become an instant billionaire by cutting costs at Google or Procter & Gamble. I would cut their advertising spend to zero and save them more than $7 billion. It would be profoundly stupid but if that was my sole incentive, it would be monumentally lucrative for me.

Despite the obviousness of the lesson, it just isn’t widely learned, and these projects keep happening. And I can just hear the claims of the smarmy cost reduction consulting partner: “Oh no, Roger. We use our strategy brilliance to ensure that the costs we cut won’t adversely impact revenues.” OK then, why don’t you include that in your contract incentive structure. “Yes, but Roger, we work closely with management to ensure that we have consensus on every single line item cut.” But that has nothing to do with why you don’t include revenue maintenance (or better yet, enhancement) in your contract incentive structure.

There is a reason revenue is nowhere to be found in the incentive structures of these gainsharing contracts. It is because increasing profit is hard while reducing costs (without concern for revenues) is as easy as fishing in a barrel. And the cost reduction consultants love nothing more than fishing in a barrel for huge heaping piles of cash. Reducing costs in a way that enhances profits is really hard. That is why companies don’t get it done on their own and look for help. I get that. But their desperation just opens them up to exploitation.

The Bottom Line

It is managerially irresponsible for executive leadership (management and board) to hire a cost reduction consultant to work for its company under an incentive agreement that pays based solely on cost reduction. I wish is wasn’t so clear, but it is.

It is not as though I don’t think cost reduction is necessary. It very often is essential. It is easy to allow corporate bloat to set in — especially if a company doesn’t have a clear strategy. The only way to know whether a particular cost item is justified is if it clearly serves the strategy. Companies that don’t have a clear strategy will eventually do badly financially and will feel the need to cut costs. But it is extremely dangerous to cut costs when you don’t have a strategy — as was so obviously the case at JC Penney — because you have no idea which are good costs, and which are bad ones. But these are the most desperate companies, who are awesome targets for the cost reduction consultants (and craven hedge fund activists).

Practitioner Insights

I have practitioner advice for four different groups, each of which is involved in different ways in cost reduction projects of the sort discussed.

For senior executives, contracting will be a challenge and you will need to rise to it. The ‘strategy consulting’ firms will tell you that what you want is not ‘how it is done,’ and that they can’t be held accountable for profitability. That is because they have discovered how rewarding it is to fish in a barrel and they don’t want you to force them to fish in the ocean. Don’t buy their line about being attentive to the revenue side when, at the same time, they refuse to ensconce that attentiveness in the contract. Hold firm for the sake of your company.

For board members, you can play a really important role. One role that boards can always play is to help management in its negotiations by saying: “No, we don’t approve.” Whether it is the price of an acquisition, the capital cost of a project, the terms of a joint venture, or anything else, you can always say: “No.” And that will help your management team overcome the above challenge. Help them. Don’t leave them to fend for themselves with the sharks.

For junior consultants working on gainsharing cost-reduction-only projects, grit it out because you don’t have much of a choice. But try hard to avoid getting assigned to another one — say that you have had that experience already and want to broaden your skillset, or some other excuse — because you will learn nothing of value to your business career working on a project as stupid and client unfriendly as this. If anything, it will make you a worse consultant. Over time, you will only be as good as your work, and this is certifiably bad work.

For company employees, if one of these happens at your company, you are the best defense against stupidity. You know the company better than any consultant can ever hope to. If they are recommending a cut that you know will create a JC Penney/Kraft Heinz outcome, push back. But at the same time, support the cuts that you know will eliminate waste and will have no negative revenue impact. Your executive leadership shouldn’t be putting this task on your shoulders but rise to the occasion anyway. Unlike the consultants, you will learn a lot by taking an integrative stance.